Factors Affecting adoption of Self service Banking in Do it for me Indian Culture

This paper aims at finding the factors affecting adoption of self service banking while testing the validity of Technology acceptance model (TAM) in India. The study collects data from 314 respondents from tier 2 cities in India and uses Structural equation modeling to test the conceptual model. The results of the study indicated that the model converged with a additional path from personal contact to attitude, and a covariance between personal contact and perceived risk; technology discomfort and capability. The results therefore, indicated that TAM was only partially applicable in India i.e. Perceived ease of Use (PEU) and perceived usefulness (PU) do act as mediating variables for two significant factors which influence the attitude towards usage of self service banking technologies. However; need for personal contact (PC) was an added dimension which was found to be significantly and negatively influencing the consumer attitude to use self service banking. The results further indicated that as the perceived risk increased the need for personal contact increased among the respondents in terms of self service banking. The covariance between technology discomfort and capability further highlighted the need for companies investing in educating the customers about “what if error was made scenario” and recovery systems. A focus on these added dimensions would lead to higher usage of self service technologies in India.

Introduction

Over past decade companies have been experimenting with sophisticated technologies in service blueprints with the primary motivation of achieving customerization in service processes. This strategy helps the companies to give transactional control to the customers. In the service industry where inseparability is a part of the very nature of industry, customerization helps the company reap additional benefits like increased efficiency of service processes, reduced cost of operations, and improved quality (Legris et al., 2003, Meuter et al., 2000).

Past research, has been dominated by understanding various aspects of the technology equation like developing understanding of the technology adoption by consumers, predicting factors leading to technology acceptance by consumers and various competitive dynamics of the technology in service blueprint. Researchers have developed various frameworks to help companies understand the factors and process that influences the consumer’s technology adoption like the theory of reasoned action (Fishbein, 1979), Technology acceptance model (Davis, 1985), task technology fit model (Goodhue and Thompson, 1995) and Innovation diffusion theory (Rogers, 2010), just to list a few.

Backed by the knowledge gained from these models service companies have invested in technologies and reorienting their service blueprints around this self service channel. This has been especially true for banking industry where the ATM, credit card, debit card, mobile banking and even the internet banking has transferred the transactional control to the customer. These technologies have given the freedom to the customer to bank anytime anywhere. Therefore, these technologies in the service blueprint were presented as a win-win scenario where the customer got flexibility, freedom and control while the company was able to reap cost and profit benefits.

However, statistics indicate that technology and service blueprint have not been as successful in India, as the companies perceived them to be. The self service banking channels are suffering from a low adoption rate in India i.e. 65% of the online banking registered customer remain inactive (public as well as private banks) and the number of registered users itself ranges between only 2% and 8% of overall number of banking transactions across all channels(EY, 2014).

When it comes to India, two variables, availability of man power and high power distance index have meant that Indian culture is more oriented towards “do it for me” culture rather than self service. In this culture introduction of a do it yourself technology requires major consumer behavior changes – which requires deeper understanding of consumer specific dynamics. It is because of this reasons that Mc Donald, KFC decided it was easier to change the service models to accommodate this orientation of the Indian culture. Therefore, even in service industry cultural context is very important to decide the tradeoff between do it yourself and do it for me models. This is where the practitioners turn to models in service literature.

However, the knowledge of the models and the technology in service blueprinting is based on findings from data set collected from a country (mostly North America) which are culturally very different from India. Therefore, generalizing usage of TAM across cultures is debatable and a risky proposition as proven by Straub and his colleagues. They tested predictability of one of the popular models, Technology Acceptance Model (TAM), across 3 countries and found that the model was not universally applicable (Straub et al., 1997).

It is within this cultural context of technology and service blueprinting that the current study has been undertaken to study factors affecting technology acceptance model in India in context of use of technology to provide customerizatiom in banking (involves ebanking, ATM, debit cards etc).

It is important to mention that there have been studies determining the factors effecting adoption of technology in India (Mukherjee and Nath, 2003, Kumra and Mittal, 2004, Khare et al., 2012, Kesharwani and Bisht, 2012, Sharma and Govindaluri, 2014, Safeena et al., 2011). Khare and her colleagues studied effect of dimension of trust and convenience on adoption of internet banking while Kumra & Mittal; Mukherjee & Nath focused on dimension of trust in internet banking. Safeena and colleagues focused on only 3 variables i.e. perceived risk, perceived ease of use and perceived usefulness. Sharma& Govindaluri; Kesharwani & Bisht studied TAM in context of India. It was found that past research focused on only one aspect of the model or extended the factors to a limited extent. The review of literature further highlighted that there is scarcity of studies which have focused on testing not only TAM but also factors which affected technology acceptance model a opinion supported by Kesharwani and colleagues(Kesharwani and Bisht, 2012). Further most of these studies referred to only internet banking and not self service banking methodologies as a whole. Given the limited resources companies have it is necessary to look for orientation which is common across channels. Use of technology across channels provides that common link and hence strategies need to be based across the communality rather than on a channel.

The current study explores TAM in respect to self service banking in India i.e. it combines all the technology oriented channels and tries to study the apprehensions of the customer in more of a general respect than specific to a product. The study premise limits itself to all banking services where self service model is being adopted but it expands external variables of TAM to include multiple constructs.

The study will help companies understand the technology adoption model in respect to India and also factors which influence the adoption of technology India. This understanding would help companies increase the adoption rate of self service banking in India. The paper will also add to the existing base of literature on TAM in India. The paper starts by discussing the framework and background for hypothesis, outlines the research methodology adopted followed by results of the study. The paper concludes by highlighting the implications and contributions of the study.

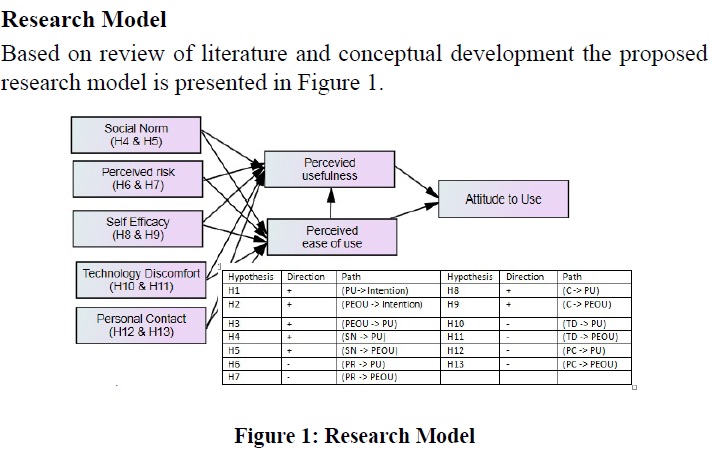

Conceptual Development

Technology Acceptance Model (TAM ): Perceived usefulness and ease of use

TAM model was proposed by Davis as a model for predicting whether users will adopt a new technology or not (Davis, 1993). TAM posits that behavioral intention (attitude) is determinant of actual use and behavioral intention is in turn determined by perceived ease of use and perceived utility which act as mediating variables for a set of external variables. Further, model states that Perceived utility is the user’s perception of the extent to which using technology would enhance their performance and perceived ease of use is perception of the user of the amount of effort required to use the technology. Many researchers have empirically proved that perceived usefulness and perceived ease of use exert a significant and positive effect on attitude towards technology adoption (Venkatesh and Davis, 2000, Henderson and Divett, 2003, Fenech, 1998). Research has also indicated that perceived ease of use could influence perceived usefulness (Kesharwani and Bisht, 2012). Therefore, in the current study the TAM is taken in its original structure which states that the perceived usefulness and perceived ease of use determine the attitude towards intention to use.

Hypothesis 1: Perceived usefulness will have positive and significant impact on individual’s Attitude to use self service banking.

(PU-> Attitude )

Hypothesis 2: Perceived ease of use will have positive and significant impact on individual’s Attitude to use self service banking.

(PEOU-> Attitude)

Hypothesis 3: Perceived ease of use will have positive and significant impact on perceived usefulness to use self service banking.

(PEOU-> PU)

The model over the years has been adapted to include a variety of external variables across cultures, economies and even industries(Legris et al., 2003, Calisir et al., 2014). These studies have tried to expand the TAM model but have comprehensively cited works which have over the years worked on defining and expanding external variables which influence perceived usefulness and ease of use of a customer. An amalgamation of these studies was used to narrow 3 categories of variables.

*Social influences/subjective norm: This set of variables refers to social factors which influence a customer to adopt self service banking. It is defined as ‘‘a person’s perception that most people who are important to him think he should or should not perform the behavior in question’’(Fishbein, 1979, Fishbein and Ajzen, 1975). Past research has indicated that there is evidence pertaining to social norm in both the directions i.e. a group of studies indicate that more than often consumers face social pressures to use innovative technology options and therefore, they have extended TAM to study influence of social influences on TAM (Davis, 1993, Wang et al., 2013, Hsu and Lu, 2004). An individual might learn to use skype because of pressure to communicate with a family member abroad. On the other hand some studies have found social norm to be an insignificant variable (Venkatesh and Davis, 2000). However, as per Hofstede India is a Collectivist culture where the group tends to be more important than the individual and the person is more likely to be concerned about the thoughts and opinions of others (Hofstede, 1980). Therefore it is argued that in India social norm would affect perceived utility of the customer. The current study extends the model to test social norm with perceived usefulness and perceived ease of use.

Hypothesis 4: Social Norm will have positive and significant impact on perceived usefulness to use self service banking.

(SN-> PU)

Hypothesis 5: Social Norm will have positive and significant impact on perceived ease of use to use self service banking.

(SN-> PEOU)

* Perceived Risk: Perceived risk refers to uncertainty regarding expected benefits from a product or service. ‘‘a combination of uncertainty plus seriousness of outcome involved’’(Bauer, 1960). Many scholars have extended TAM to include perceived risk especially in case of information processing industries (Lee, 2009, Kesharwani and Bisht, 2012, Featherman and Pavlou, 2003, Yiu et al., 2007). Past research indicates that Perceived risk directly influences the adoption of innovative technology (Kumar and Dange, 2014). Kansal indicates that the adoption of online purchase in India is greatly influenced by perceived risk and privacy concerns(Kansal, 2014). Kumar and Dange indicate that the buyers have maximum perceived risk regarding financial risk, social risk, time risk and security risk(Kumar and Dange, 2014). Given the high information processing nature of banking industry the perception of financial and security risk is expected to be high. Therefore, it is argued that as the perception of perceived risk increases the customers would have a more negative perception regarding utility of the technology (self service banking options) and perceived ease of use and therefore are less motivated to adopt the technology.

Hypothesis 6: perceived risk will have negative and significant impact on perceived usefulness to use self service banking.

(PR -> PU)

Hypothesis 7: perceived risk will have negative and significant impact on perceived ease of use to use self service banking.

(PR -> PEOU)

*Individual Differences: Review of literature indicated that another category of variables which influenced adoption of technology was individual differences. These include variables like self efficacy or capability, technology discomfort and personal contact.

Self efficacy/Capability: Social learning theory states that ‘‘psychological procedures, whatever their form, alter expectations of personal efficacy’’ (Bandura, 1977). In case of an individual expectations and perceptions of personal efficiency, determine individuals decisions regarding what actions to take, how much effort to invest and how long to try and what strategies to use to deal with a challenge (Yi and Hwang, 2003, Igbaria and Iivari, 1995, Chau, 2001). Igbaria and colleagues (1995) extended technology acceptance model (TAM) to incorporate role of capability in computer usage and found that self efficacy had direct and indirect effect on perceived usefulness. It was perception of self efficacy which determined the effort a customer was ready to put in to learn the technology and technology oriented service else he would use the defense mechanism and argue that the technology is not useful enough for him to put in the effort. Therefore, it is argued that if an individual perceives that he is capable of learning technology oriented banking service then he would perceive the technology to be easy to use and would also have higher perception of usefulness of that technology.

Hypothesis 8: Capability will have positive and significant impact on perceived usefulness to use self service banking.

(C -> PU)

Hypothesis 9: Capability will have positive and significant impact on perceived ease of use to use self service banking.

(C -> PEOU)

Technology Discomfort: Technology discomfort is referred to as the tendency of an individual to be uneasy, apprehensive, stressed or have anxious feelings about the use of technology (Venkatesh, 2000). Technology discomfort is a dimension of technology readiness which was developed to measure general beliefs about technology through optimism, innovativeness, discomfort and insecurity (Parasuraman, 2000). In case of self service banking technologies, technology discomfort and insecurity are the major inhibitors of adoption of technology(Lin and Hsieh, 2007). Past research has indicated that there is a negative effect of technology discomfort on perceived ease of use and perceived usefulness(Venkatesh, 2000, Rose and Fogarty, 2006). The results indicate that higher is the technology discomfort experienced by a customer more would be his apprehensions in terms of learning the technology oriented service and hence lesser would be his perceived ease of use and utility of the service. Therefore, it is argued that higher is the technology discomfort lesser would be perceived ease of use. The current study extends the model is extended to test technology discomfort with perceived usefulness.

Hypothesis 10: Technology discomfort will have negative and significant impact on perceived usefulness to use self service banking.

(TD -> PU)

Hypothesis 11: Technology discomfort will have negative and significant impact on perceived ease of use to use self service banking.

(TD -> PEOU)

Personal Contact: personal contact refers to need for interaction with the service provider. Curran and Meuter extended the TAM to include need for interaction (Curran and Meuter, 2005). Past research has established that higher is the desire for personal attention more is the inclination of the individual to opt for face to face interactions (Saxena et al., 2015). Therefore, a customer who desires higher degree of personal contact and attention would avoid using self service banking and therefore would have lesser perceived usefulness. Furthermore, India has traditionally been a labor intensive production process country and the same philosophy was carried forward to service processes as well. This implied that India became more of a do it for me culture. Therefore, perception of ease of use of a channel where someone does something for u is higher. The current study extends the model is extended to test personal contact with perceived ease of use. It is hypothesized that there would be a negative relationship between the two.

Hypothesis 12: Personal contact will have negative and significant impact on perceived usefulness to use self service banking.

(PC -> PU)

Hypothesis 13: Personal contact will have negative and significant impact on perceived ease of use to use self service banking.

(PC -> PEOU)

Research Methodology

To test the proposed hypotheses, a survey was done and data were collected from 314 respondents. The population of the study was customers in India. Inorder to choose a sample a two stage sampling procedure was followed. Reports indicate that the next phase of economic boom is in Tier II cities (Singh, 2015) Therefore, it was decided to choose the sample from tier II cities rather than Metropolitans. In stage 1 it was decided to choose 4 tier 2 cities in India. The sampling frame was defined as 26 Tier 2 cities of India. The sampling frame was generated from a list of tier 2 cities, which was based on grading structure devised by the Government of India to allot House Rent Allowance (HRA). Data was collected by mall/ market intercepts in four cities i.e. Chandigarh, Ahmedabad, Dehradun and Ludhiana. Data was collected from 80 respondents in each city and the total usable questionnaire were 314.

Data was collected using a structured non disguised questionnaire. The questionnaire had 8 sections dealing with independent and dependent variables and additional two sections for collecting response to demographic variables and their use of existing banking technologies. Standardized scales were used to collect data for 7 variables included in the study i.e. Perceived Usefulness and Perceived ease of Use (Davis, 1985); Technology discomfort (Parasuraman, 2000); Subjective norm (Taylor and Todd, 1995); Perceived risk(Parasuraman, 2000); Self efficacy (Chen et al., 2001); Personal Contact (Walker et al., 2002, Dabholkar, 1996) and the items for attitude towards intention to use were developed.

The sample consisted of respondents aged between 20 -70 years. Among 314 respondents, 39.2 per cent of the total respondents were in their 20s, 30.3 per cent in their 30s, 10.2 and 11.5 per cent in their 40s and 50s respectively and 7 percent were in their 60s. Among the respondents, 60.2 per cent of the total respondents were males and around 40 per cent of the total respondents were female. Majority of the respondents (86.9 per cent) had been using some form of self service banking. 58.2 percent of the respondents had been using self service banking for 3- 8 years. Interestingly except for ATM which was being used by majority of respondents around 60-70 percent times other methods like the debit card, credit card and mobile banking was being used only 10-20 per cent of times. Thereby, indicating reluctance of the sample for self service banking methodologies and making them adequate for the study.

Psychometric properties of scale

Following previous research, the analysis of the psychometric properties of the instrument included an analysis of its content validity, face validity, reliability and factor structure (Kostova and Roth, 2002, Bagozzi et al., 1991).

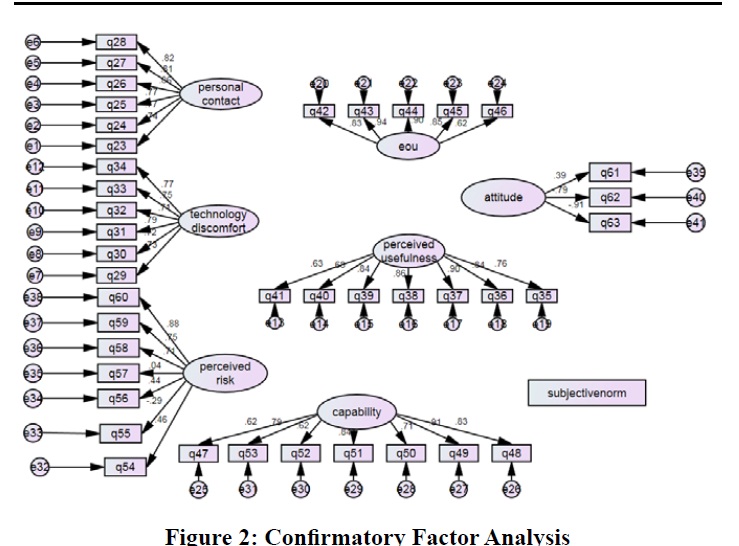

Face validity and content validity: The survey instrument was written in English and was pre-tested on a small sample of 20 respondents. Face validity and content validity of the instrument and its items were concluded by various researchers with experience in conducting surveys. The analysis of factor structure was undertaken through confirmatory factor analysis (CFA).

Confirmatory Factor Analysis (CFA): CFA was used to assess convergent and Discriminant validity of each construct. A standardized path analysis was generated (Figure 2). In order to improve convergent validity of the model some of the items needed to be deleted. Therefore, it was decided to delete items which loaded on a construct at a value less than 0.40 as suggested by past research (Costello and Osborne, 2011). An analysis of results of CFA indicated that for personal contact, capability, perceived usefulness, attitude, ease of use and technology discomfort all items were above decided loading of 0.40, for perceived risk 2 items were less than decided communality of 0.40 and therefore two items were deleted from the scale i.e. q55 and q57.

Under construct validity convergent validity was done to check if the measures of each construct within the model were reflected by their own indicators and Discriminant validity was done to check if the of the different concepts were statistically different (Gefen et al., 2000, Hair, 2010). The Composite reliability (CR) values of the model were greater than average variance explained (AVE); and AVE values were greater than 0.50; maximum shared squared variance (MSV) values were less than AVE, and average shared squared variance (ASV) values were less than the AVE indicating that there was Discriminant and convergent validity (Hair Jr et al., 2010).

As the scales were adapted the reliability of the scale was tested with help of Cronbach Alpha. The data was also checked for multicollinearity across independent variables. There indicated to be no multicollinearity issues among the independent variables as suggested by Tabachnick, & Fidell (Tabachnick and Fidell, 2001).

Reliability Cronbach Aplha: The internal consistency and reliability of the scale was measured using Cronbach coefficient alpha. According to works of Nunnally, 1978, for purpose of basic research, a Cronbach alpha of 0.70 or higher is sufficient (Nunnally, 1978). Cronbach alpha for the adopted scale met this limit. It was found that a Cronbach alpha value for all constructs was higher than .70. The Cronbach Alpha for personal contact was 0.911, technology discomfort was 0.881, perceived utility was 0.921, perceived ease of use 0.917, capability 0.905 and perceived risk 0.822.

Results and Discussion

Model 1: the first model estimated that perceived usefulness and perceived ease of use mediates the relationship between personal contact, technology discomfort, perceived risk, capability, subjective norm and attitude. The first model also estimated that there was influence of perceived ease of use on perceived usefulness (figure 3). The chi square for the model did not support the model (=2482.060, df = 807, p=0.000). The value indicated that there was a possible difference between the model’s implied population covariance and actual observed covariance’s. However, researchers have suggested that is sensitive to sample size and therefore should not be solely used to accept or reject or accept a model (Fornell and Larcker, 1981). A model can be accepted if it passes at least 3 fit indices (Bollen and Long, 1993, Jaccard, 1996). Therefore, an overall fit was estimated using 3 category of indices i.e. absolute fit indices, incremental fit indices and parsimonious fit indices (table 2).

The, GFI, RMSEA, NFI, CFI, AGFI and normed chi square indicated that model was not a very good fit and could be improved. An analysis of the, modification indices indicated that a covariance between technology discomfort and capability, the discrepancy will fall by at least 147.052. Additionally, a direct path between personal contact and attitude, would lead to decrease in the discrepancy by 21.646. The model suggested that there would be a negative covariance between capability and technology discomfort. Literature was reviewed to search for support for these proposed paths. Research indicated that many older individuals because of their limited exposure to technology especially internet, experience anxiety when they have to use these technologies and therefore choose to avoid these because of perceived difficulty (Porter and Donthu, 2006).

If a consumer perceives that they have used a similar technology before successfully and had the necessary expertise to learn the technology use, then they would be more ready to learn it. Therefore, indicating that a consumer’s personal beliefs about capability do have an influence on the technology learning related anxiety. Personal contact as a dimension was added to this model to explore the impact of technology on customer relationship management. In India the additional path could be explained on the basis of it being a culture of “do it for me”. India is a “we” economy where businesses are based on relationships. Customers use this variable to decrease the perception of risk.

India is traditionally a do it for me economy. The cultural conditioning starts from early years where household help does a lot of chores for people. Same habits and expectations are carried forward to the purchase behavior where people expect customer contact employees to do things for them. A testimony to this behavior is the changed business service model of companies like Mcdonald which are ode to self service. Therefore, when a customer contact employee performs the facilitating steps required to consume the service the attitude towards self service banking should decrease. The modifications indices suggested a negative relationship between personal contact and attitude.

Therefore, additional paths were added i.e. personal contact -> attitude and Technology Discomfort <-> capability and test the resulting model 2. The chi square for the new model changed by 456.135, though the null hypothesis was still rejected indicating that the model was not a good fit. However, the three indices indicated that the model was a better fit than the earlier specified model. An analysis of the revised modification indices indicated that additional paths could improve the model fit. An additional covariance path from perceived risk to personal contact would decrease the discrepancy by 43.703.

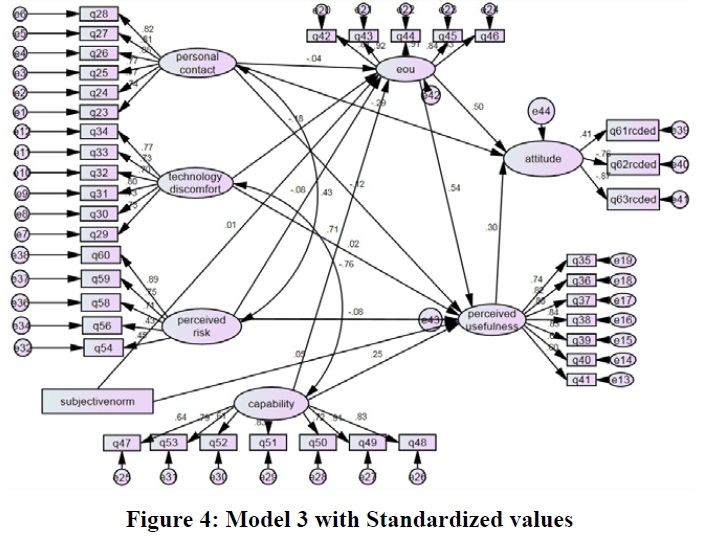

Thus, an additional path was defined i.e. personal contact <-> perceived risk resulting in model 3.

The fit indices for Model 3 indicated that though the chi square still did not support the model fit yet the normed chi square (2.72) was within acceptable limit of 1 to 3. Normed chi square is not sensitive to sample size and therefore has been referred to as a better indice for judging model fitness by some (Hooper et al., 2008). Therefore, model was acceptable as per parsimonious indices. As per absolute indices the RMSEA was at (0.07) which was well within the acceptable limit or 0.05 to 0.080 and GFI was at 0.80. Therefore, the absolute fit indices were from moderate to good. Incremental fit indices indicated moderate to good fit for the model that NFI was 0.80, CFI was 0.90 and AGFI was 0.80.

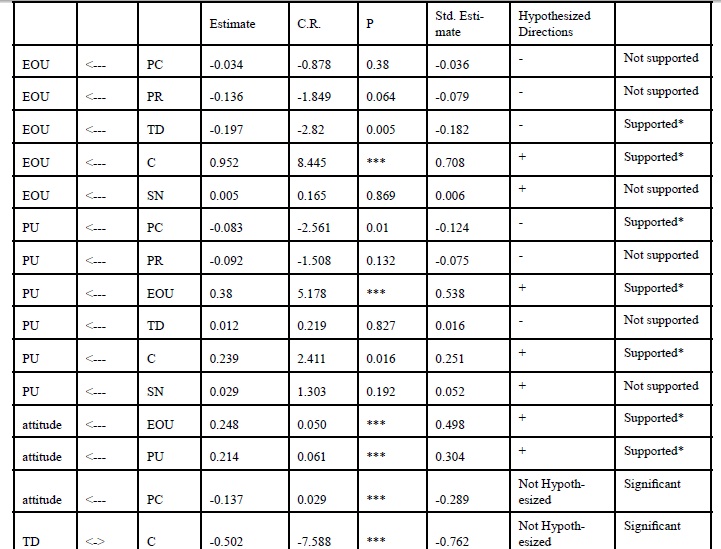

The hypotheses were tested in model 3. The regression results for the model indicated that the 8 paths were significant and were supported. Data supported technology discomfort to EOU and capability to EOU. PC and C was also significantly related to PU. EOU was significantly related to PU (TABLE 3). As expected EOU and PU were related to attitude therefore, there was some mediating effect between these variables. Interestingly which was different for TAM in India was a direct effect of PC on attitude.

Table 3: Regression Results and hypothesis

Therefore, in conclusion results indicated that a part of TAM was valid in India as well i.e. perceived usefulness and perceived ease of use were mediating variable for external variables and there was a significant relationship between perceived ease of use and perceived usefulness. However, some divergence was also found in the conventional model where perceived usefulness and ease of use were not mediating effect of all the variables. Personal contact was found to be an important variable which affected the consumer’s attitude towards intention to use self service banking. Results in India also supported that there was also a positive covariance between perceived risk and personal contact indicating that increase in perceived risk indicated increased perception of personal contact. The results also indicated that there was a negative covariance between technology discomfort and capability.

Discussion and implications

The results indicated that TAM did not apply in its original format to India in terms of self service banking technologies. The model was accepted with some additional paths i.e. personal contact to attitude. There was a negative relationship between need for personal contact and attitude to use self service banking in India indicating that the biggest hurdle to adoption of self service banking technologies was the need for personal contact in Indian culture. This could be explained on basis of relationship between the perceived risk and personal contact. As the perceived risk of the self service channel increased the customer turned to an expert or the person who dealt in the service on a daily basis to reduce the perceived risk. Therefore, the increase the adoption of the self service banking technologies it is important for the bankers to invest in decreasing the perceived risk that is associated with self service technologies. The banks need to invest in increasing the customer trust in banking systems and especially recovery procedures especially in case an error has been made. Further, there was a positive relationship between capability and perceived usefulness. The results indicated that in India companies need to invest in terms of educating people and making them more comfortable and confident about their capability to use the technology.

The results further indicated that there was a negative relationship between technology discomfort and ease of use and a positive relationship between capability and ease of use. This indicates that the as the respondents felt confident about their capability to use a technology oriented self service banking facility their perception about the ease of use of that channel also increased leading to a more positive attitude and inturn an intention to use. An increased faith in capability also led to a decrease in technology discomfort. Therefore, the bankers additionally need to invest in educating people to the simplicity of the technology and more than that making them less scared of error scenarios. Strategies like free trial with technology, trial and error encouragement and assured fail safe mechanism could help companies achieve this objective. To achieve this objective customer need to be taught how managing financing by self is less riskier proposition. This set of results is unique to Indian culture and banks and financial institutions need to understand this aspect and then approach marketing self service banking from a different dimension. One of the possible reasons for self service banking not being successful is that banks continue to cater to personal contact whims of the customers and use self service banking facilities as complimentary services rather than a substitute distribution channel.

Conclusion

The current study tests the Technology acceptance model in India and identifies the external factors which influence attitude towards intention to use self service banking technologies. TAM has been found to partially applicable in India. PEU and PU do act as mediating variables however; PC was an added dimension which influenced the attitude of intention to use self service banking directly. Furthermore, there was a covariance between technology discomfort and capability and perceived risk and personal contact. Therefore, the increase the adoption of the self service banking technologies it is important for the bankers to invest in decreasing the perceived risk that is associated with self service technologies. The banks need to invest in increasing the customer trust in banking systems and especially recovery procedures especially in case an error has been made. A focus on these added dimensions in India would lead to higher usage of self service technologies in India.

References

Bagozzi, R.P., Yi, Y. & Phillips, L.W. (1991) ‘Assessing construct validity in organizational research’. Administrative science quarterly, pp 421-458.

Bauer, R.A., (1960) Consumer Behavior as Risk Taking, Dynamic Marketing for a Chasing World, Robert S. Hancock, Chicago: American Marketing Association, pp.38-398..

Bollen K.A. & Long J.S. (1993) Testing Structural Equation Models., Newbury Park, Sage Publications.

Calisir, F., Altin Gumussoy, C., Bayraktaroglu, A.E. & Karaali, D. (2014) ‘Predicting the Intention to Use a Web Based Learning System: Perceived Content Quality, Anxiety, Perceived System Quality, Image, and the Technology Acceptance Model.’ Human Factors and Ergonomics in Manufacturing & Service Industries, 24:5, pp. 515-531.

Chau, P.Y. (2001) ‘Influence of computer attitude and self-efficacy on IT usage behavior’, Journal of Organizational and End User Computing (JOEUC), 13:1, pp 26-33.

Chen, G., Gully, S.M. & Eden, D. (2001) ‘Validation of a new general self-efficacy scale’, Organizational research methods, 4:1, pp 62-83.

Osborne, J. W., & Costello, A.B. (2009) ‘Best practices in exploratory factor analysis: Four recommendations for getting the most from your analysis’, Pan-Pacific Management Review, 12:2, pp 131-146.

Curran, J.M. & Meuter, M.L.(2005) ‘Self-service technology adoption: Comparing three technologies’. Journal of Services Marketing, 19:2:, pp 103-113.

Dabholkar, P.A. (1996) ‘Consumer evaluations of new technology-based self-service options: An investigation of alternative models of service quality’, International Journal of research in Marketing, 13:1, pp 29-51.

Davis Jr, F.D., (1986) A technology acceptance model for empirically testing new enduser information systems: Theory and results (Doctoral dissertation, Massachusetts Institute of Technology).

Davis, F.D. (1993) ‘User acceptance of information technology: System characteristics, user perceptions and behavioral impacts’, International Journal of Man-Machine Studies, 38, pp 475-487.

Ernst & Young LLP and Indian Banks Association (2014) Banking on Technology: Perspectives on the Indian Banking Industry (online) (1 January 2015). Available from URL:<http://www.ey.com/Publication/vwLUAssets/EY-Banking-on-Technology/$FILE/EY-Banking-on-Technology.pdf>.

Featherman, M.S. & Pavlou, P.A. (2003) ‘Predicting e-services adoption: A perceived risk facets perspective’, International Journal of Human-Computer Ctudies, 59:4, pp. 451-474.

Fenech, T. (1998) ‘Using perceived ease of use and perceived usefulness to predict acceptance of the World Wide Web’, Computer Networks and ISDN Systems, 30:1-7, pp. 629-630.

Fishbein, M. (1979) A theory of reasoned action: Some applications and implications, Nebr Symp Motiv, 9:27, pp. 65-116.

Fishbein, M. & Ajzen, I. (1975) Belief, attitude, intention and behavior: An introduction to theory and research. Addison Wesley: MA.

Fornell, C. & Larcker, D.F. (1981) ‘Evaluating structural equation models with unobservable variables and measurement error’, Journal of marketing research, pp 39-50.

Gefen, D., Straub, D. & Boudreau, M.C. (2000) ‘Structural equation modeling and regression: Guidelines for research practice.’ Communications of the association for information systems, 4:1, pp 7.

Goodhue, D.L. & Thompson, R.L. (1995) ‘Task-technology fit and individual performance’, MIS quarterly, pp 213-236.

Hair, J.F. et-al (2010) Multivariate data analysis (7th Edn) Pearson.

Hair, J.F., Anderson, R.E., Babin, B.J. and Black, W.C., 2010. Multivariate data analysis: A global perspective (Vol. 7) Upper Saddle River, NJ: Pearson., pp 629-686.

Henderson, R. & Divett, M.J. (2003) ‘Perceived usefulness, ease of use and electronic supermarket use’’ International Journal of Human-Computer Studies, 59:3, pp 383-395.

Hofstede, G. 1980 ‘Culture’s consequences: National differences in thinking and organizing’. Beverly Hills, Calif.: Sage.

Hooper, D., Coughlan, J. & Mullen, M. (2008) ‘Structural equation modelling: Guidelines for determining model fit’. Dublin Institute of Technology- ARROW@DITArticles. (online) (2 December 15). Available from URL:<http://arrow.dit.ie/cgi/viewcontent. cgi?article=1001&context=buschmanart>

Hsu, C.L. & Lu, H.P. (2004) ‘Why do people play on-line games? An extended TAM with social influences and flow experience’. Information & Management, 41(7), pp 853-868. Igbaria, M. & Iivari, J. ( 1995) ‘The effects of self-efficacy on computer usage’. Omega, 23(6), pp 587-605.

Jaccard J. & K., W.C. (1996) LISEREL Approaches to Interaction Effects in Multiple Regression, Thousands Oaks, CA, Sage publications.

Kansal, P. (2014) ‘Online privacy concerns and consumer reactions: insights for future strategies’, Journal of Indian Business Research, 6:3, pp 190-212.

Kesharwani, A. & Bisht, S.S. (2012) ‘The impact of trust and perceived risk on internet banking adoption in India: An extension of technology acceptance mode’l. International Journal of Bank Marketing, 30:4, pp 303-322.

Khare, A., Mishra, A. & Singh, A. B. (2012) ‘Indian customers’ attitude towards trust and convenience dimensions of internet banking’, International Journal of Services and Operations Management, 11:1, pp 107-122.

Kostova, T. & Roth, K. (2002) ‘Adoption of an organizational practice by subsidiaries of multinational corporations: Institutional and relational effects’, Academy of Management Journal, 45:1, pp 215-233.

Kumar, V. & Dange, U. (2014) ‘A Study on Perceived Risk in Online Shopping of Youth in Pune: A Factor Analysis’. Available at SSRN 2518293.

Kumra, R. & Mittal, R. (2004) ‘Trust and its Determinants in Internet Banking: A Study of Private Sector Banks in India’ Decision (0304-0941), 31:1, pp. 73-96.

Lee, M.C. (2009) ‘Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit’, Electronic Commerce Research and Applications, 8:3, pp. 130-141.

Legris, P., Ingham, J. & Collerette, P. (2003) ‘Why do people use information technology? A critical review of the technology acceptance model’, Information & management, 40:3, pp 191-204.

Lin, J.S.C. & Hsieh, P.L. (2007) ‘The influence of technology readiness on satisfaction and behavioral intentions toward self-service technologies’, Computers in Human Behavior, 23:3, pp 1597-1615.

Meuter, M.L., Ostrom, A.L., Roundtree, R.I. & Bitner, M.J. (2000) ‘Self-service technologies: Understanding customer satisfaction with technology-based service

encounters’, Journal of Marketing, 64:3, pp. 50-64.

Mukherjee, A. & Nath, P. (2003) ‘A Model of trust in online relationship banking’, International Journal of Bank Marketing, 21:1, pp. 5-15.

Nunnally, J.C. (1978) Psychometric theory, New York, McGraw-Hill.

Parasuraman, A. (2000) ‘Technology Readiness Index (TRI) a multiple-item scale to measure readiness to embrace new technologies’ Journal of service research, 2:4, pp. 307-320.

Porter, C.E. & Donthu, N. (2006) ‘Using the technology acceptance model to explain how attitudes determine Internet usage: The role of perceived access barriers and demographics’ Journal of business research, 59:9, pp. 999-1007.

Rogers, E.M. (2010) Diffusion of innovations, Simon and Schuster.

Rose, J. & Fogarty, G.J. (2006) ‘Determinants of perceived usefulness and perceived ease of use in the technology acceptance model: senior consumers’ adoption of self-service banking technologies’. Proceedings of the 2nd Biennial Conference of the Academy of World Business (online) (2 December 2014). Available from URL:<https://www.researchgate.net/publication/242164302_DETERMINANTS_OF_PERCEIVED_USEFULNESS_AND_PERCEIVED_EASE_OF_USE_IN_THE_TECHNOLOGY_ACCEPTANCE_MODEL_SENIOR_CONSUMERS’_ADOPTION_OF_SELFSERVICE_BANKING_TECHNOLOGIES>

Safeena, R., Date, H. and Kammani, A., (2011) ‘Internet Banking Adoption in an EmergingEconomy: Indian Consumer’s Perspective’. Int. Arab J. e-Technol., 2:1, pp.56-64.

Saxena, R., Sinha, M. and Majra, H., (2015) Self-service technologies: building relationships with Indian consumers. Handbook on Research in Relationship Marketing, p.177.

Kumar Sharma, S. and Madhumohan Govindaluri, S., (2014) ‘Internet banking adoption in India: structural equation modeling approach’, Journal of Indian Business Research, 6:2, pp. 155-169.

Singh, S. (2015) ‘Emerging Trends: Tier II, III cities set to grow in next phase of economic boom’ The Indian Express, Feb 14.

Straub, D., Keil, M. and Brenner, W., (1997) ‘Testing the technology acceptance model across cultures: A three country study’ Information & Management, 33:1, pp. 1-11.

Tabachnick, B.G., Fidell, L.S. and Osterlind, S.J., (2001) Using multivariate statistics (6th Edn), Pearson. Taylor, S. and Todd, P.A., (1995) ‘Understanding information technology usage: A test of competing models’ Information systems research, 6:2, pp. 144-176.

Venkatesh, V. (2000) ‘Determinants of perceived ease of use: Integrating control, intrinsic motivation, and emotion into the technology acceptance model’. Information systems research, 11:4, pp. 342-365.

Venkatesh, V. and Davis, F.D. (2000) ‘A theoretical extension of the technology acceptance model: Four longitudinal field studies’, Management Science, 46:2, pp. 186-204.

Walker, R.H., Craig-Lees, M., Hecker, R. and Francis, H. (2002) ‘Technology-enabled service delivery: An investigation of reasons affecting customer adoption and rejection’ International Journal of Service Industry Management, 13:1, pp. 91-106.

Wang, Y., Meister, D.B. and Gray, P.H., (2013) ‘Social influence and knowledge management systems use: Evidence from panel data’ Mis Quarterly, 37:1, pp. 299-313.

Mun, Y.Y. and Hwang, Y. (2003) ‘Predicting the use of web-based information systems: self-efficacy, enjoyment, learning goal orientation, and the technology acceptance model’, International Journal of Human-Computer Studies, 59:4, pp. 431-449.

Yiu, C.S., Grant, K. and Edgar, D., (2007) ‘Factors affecting the adoption of Internet Banking in Hong Kong—implications for the banking sector’ International Journal of Information Management, 27:5, pp. 336-351.

Dr. Purva Kansal, Assistant Professor, University Business School, Panjab University, India. Email:purvakansal@pu.ac.in; f13purvak@iimahd.ernet.in.

Recent Comments